How to Title Assets to a Trust to Avoid Probate in Colorado

You did the hard part. You sat with an attorney, made decisions about your family, your finances, and your future—and you signed a revocable living trust. Congratulations. Now comes the part most people skip and the part that Claude and ChatGPT cannot do for you: actually putting your assets into the trust.

This process is called funding your trust, and it matters more than most people realize. A trust that isn't funded is like a safe with no valuables inside—beautiful and well-built, but not doing the job.

Here's what you need to know about how to properly title assets to your trust, asset class by asset class.

First: Why Does Titling Matter?

A revocable living trust only controls what's in it. Assets titled in your name alone—without a beneficiary designation and outside the trust—will likely go through probate when you die, regardless of whether you had a will. That means court involvement, public records, potential delays, and legal fees.

→ What Happens If You Die Without a Will in Colorado?

→ How to Avoid Probate in Colorado (2026 Guide)

The entire point of most living trusts is to avoid probate. But that outcome is only possible if your assets are properly titled to the trust before you die.

The core rule is simple: the trust must appear as the legal owner—or named beneficiary—of an asset for the trust to control what happens to it at death.

How to Title Trust Assets: The Basics

When you transfer an asset to your revocable living trust, you're changing the legal ownership from "you" to "you as trustee of your trust,” while retaining beneficial ownership (i.e. the right to revoke and control the trust asset during your life). The typical titling language looks like this:

John Doe and Jane Doe, Trustees of the Doe Family Revocable Living Trust dated January 1, 2026, or any successor trustee(s) thereunder

The exact language varies by state, institution, and asset type—but the key is that the trust is identified by name and date, and you appear in your capacity as trustee, not as an individual. Keep in mind that slight variations in naming requirements are generally immaterial.

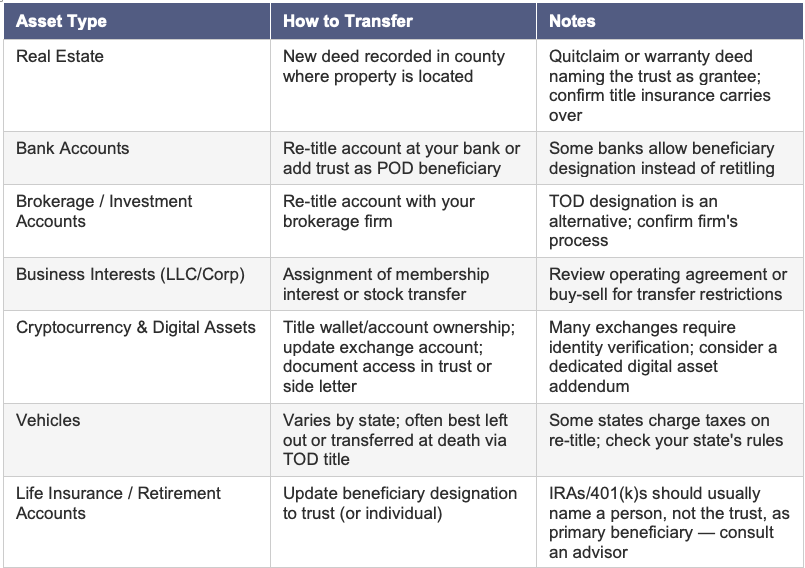

Asset-By-Asset Guide

Below is a quick-reference overview of how titling (or beneficiary designation) works for common asset types. Note that rules vary by state—always confirm with your attorney or financial institution.

Asset-By-Asset Guide for Re-Titling Assets into a Revocable Living Trust

Real Estate

Transferring real estate into a trust requires a new deed—typically a quitclaim deed or a warranty deed—that names the trust as the new owner. This deed must be recorded in the county where the property is located.

A few things to check before you transfer:

• Title insurance: Confirm your title insurer will extend coverage to the trust. Most reputable insurers do this routinely for revocable trusts, but you need written confirmation.

• Due-on-sale clauses: Federal law (the Garn-St. Germain Act) protects transfers of a primary residence into a revocable trust from triggering mortgage acceleration. Investment or second properties may be different, so be sure to check with your lender.

• Homestead exemptions: Some states require an affidavit or additional filing to preserve a homestead exemption after a transfer. Colorado, Florida, Pennsylvania, and Ohio each have different rules.

Bank and Investment Accounts

For bank and brokerage accounts, contact the institution directly. Most banks and brokerages have a dedicated process for retitling accounts into a trust name. You'll typically need to bring:

• A copy of your trust certificate or trust excerpt (not the full document)

• Identification

• Any institution-specific forms

An alternative for some accounts—especially bank savings or checking—is to add the trust as a payable-on-death (POD) beneficiary rather than retitling. This achieves a similar result but check with your attorney about which approach your plan contemplates.

Business Interests

If you own membership interests in an LLC or shares in a corporation, you can transfer those interests to your trust. The mechanism depends on the entity:

• LLC: An assignment of membership interest, signed in both your individual and trustee capacity, is typically sufficient. Just be sure to update the company's records accordingly.

• Corporation: A stock transfer is executed on the stock certificate (if certificated) or recorded in the corporation's books.

Critically: review your operating agreement or shareholders' agreement first. Many have transfer restrictions or require consent from other members before interests can be assigned. Once again, your attorney should review this before any transfer.

Bitcoin, Cryptocurrency, and Digital Assets

This is where most estate plans fall short.

Cryptocurrency and other digital assets don't transfer through a deed or a beneficiary form. Title in the traditional sense doesn't exist. What matters is who controls the private key, who has the credentials, and what legal authority does your successor trustee have to access those assets after you're gone?

→ Bitcoin Inheritance Planning: Navigating the Great Wealth Transfer in 2026

→ Apple Legacy Contact Explained: How to Give Loved Ones Access to Your iPhone After You Die

Properly planning for digital assets typically involves:

• Updating exchange account ownership or beneficiary designations where the platform allows (e.g., Coinbase)

• Documenting asset inventory, wallet types, and access instructions in a secure, trust-linked format (particularly for cold wallets)

• Granting specific trustee powers in the trust document itself to hold, manage, and transfer digital assets

• In some cases, a digital asset addendum or memorandum that can be updated without amending the trust

Note: Generic trust documents often lack the specific authority needed for a successor trustee to access or transfer cryptocurrency. If your trust was drafted without digital assets in mind, it may be worth a review.

Retirement Accounts and Life Insurance:

Here's an area where the conventional wisdom is: don't automatically title these to the trust - although there are some exceptions.

IRAs, 401(k)s, and similar retirement accounts generally pass by beneficiary designation—not through your trust and not through probate. Naming a trust as the primary beneficiary of a retirement account can create serious income tax problems for your heirs, including compressed distribution timelines under the SECURE Act.2.0

The better approach for most people is as follows:

• Name your spouse as primary beneficiary of retirement accounts

• Name individuals (children, etc.) or a specially drafted "see-through" trust as contingent beneficiaries

• Coordinate with your financial advisor on the tax implications

Life insurance works similarly. The death benefit passes by beneficiary designation. Whether to name your trust as beneficiary depends on your estate size, tax situation, and the needs of your beneficiaries. Your attorney and financial planner should work through this together.

Vehicles

Vehicles are often excluded from trust funding—not because they can't be transferred, but because the practical benefits are limited and the process varies significantly by state. Some states charge transfer fees or taxes when re-titling a car. Others offer a simple transfer-on-death (TOD) title designation.

Most estate planning attorneys suggest leaving vehicles out of the trust and relying on a pour-over will to capture any vehicle assets at death, or using a TOD designation where available.

Final Thoughts

If you want to avoid probate, make things easy for your family, and ensure nothing slips through the cracks, proper funding of your revocable living trust is critical to ensuring your assets can be efficiently transferred to the next generation.

FAQS ABOUT FUNDING REVOCABLE LIVING TRUSTS IN COLORADO

Q1: Does titling assets in a trust avoid probate?

Yes - but only if the assets are properly transferred into the trust.

Q2: Are beneficiary designations enough to avoid probate?

Sometimes, but they don’t provide control, coordination, or protection like retitling the asset to a trust might provide.

Q3: What happens if one asset is titled incorrectly?

That asset may still go through probate—even if everything else is structured properly.

Q4: Should everything go into a trust?

Not always. Certain types of assets - like retirement accounts and life insurance - typically stay outside the trust but coordinate with it.

Q5: How often should I review asset titling?

At least once per year, after major life events, and after opening new accounts.

FutureProof Law, L.L.C. is a private wealth and estate planning virtual law firm focused on helping affluent Millennials, Bitcoiners, and forward-thinking families protect their privacy, portability, and sovereignty in the digital age. Founded in 2026 by Attorney Jake Bruner, FutureProof Law, L.L.C. prioritizes an underserved generation of worried clients building wealth and legacies in a modern world. Through the preparation of creative and compassionate, digitally-native estate plans, FutureProof Law, L.L.C. helps the next generation of clients in Colorado, Florida, Ohio, and Pennsylvania seize control of their lives and legacies on the cusp of the largest transfer of wealth in history. To begin planning your future, book your FutureProof Planning Session today or contact Jake Bruner directly by phone (303-962-0625) or email (jake@futureproof.law).